This week we expand on the Energy Technology component of our Geopolitical Super Vol framework we introduced last week (here). The massive unmet energy needs of the other seven billion people on Earth were already driving investment in new energy technologies in particular for countries not blessed with sufficient domestic resources like crude oil, natural gas, or coal. A backdrop of structurally increased geopolitical uncertainty and turmoil, in particular amongst the largest economies in the world, will drive a doubling, tripling, and quadrupling down on a wide swath of new technologies that help meet energy needs. For The Lucky 1 Billion of Us, there is a need to invest in the technologies that allow our industries to compete in a host a new areas and to no longer simply cede all manufacturing to China and other Asian countries—as the U.S. and Western Europe have done over the past 25 years.

The new technology areas we are most interested in span four broad buckets:

- Grid optimization and enhancement

- Power generation

- Demand diversification opportunities, which encompasses areas like EVs (electric vehicles), LNG (liquefied natural gas) trucks, and energy efficiency

- Manufacturing and industrial competitiveness via physical AI, robotics, and automation

In this post we:

- differentiate between “Energy Tech,” which we believe has a very favorable outlook, and “Climate Tech,” the latter of which always seemed non-sensical to us.

- highlight the key areas we are watching most closely within the new technology buckets noted above.

- provide a progress report on hyperscaler profitability given the massive ramp in CAPEX seen by those companies.

- highlight Aramco as an AI and technology leader.

The opportunity for investment spans a broad spectrum of companies, technologies, and regions across a range of sectors including technology, industrials, traditional energy, new energies, power, infrastructure, metals, minerals, and mining. In a nutshell, Energy & Power + Technology + Industrials + Metals & Materials convergence.

Energy Tech versus Climate Tech

We differentiate between what we will collectively call “Energy Tech” and what many were calling “Climate Tech” over the prior 4-5 years. We were not and are not believers that “Climate Tech” is a thing. The idea that a business could generate competitive returns and growth by prioritizing reduced carbon emissions always seemed non-sensical to us.

New energy sources and technologies by definition use significantly less direct crude oil, natural gas, and coal than traditional areas. To scale, those technologies need to offer some combination of superior costs or performance or provide some other attribute like geopolitical security that governments will prioritize. There is not a person or government on Earth that does not prioritize energy availability and reliability followed closely by affordability over all other attributes. No amount of pressure campaigns—whether well- or ill-intentioned—was ever going to change that fact.

We would differentiate what we might call “Regulatory Tech” from that broader notion of Climate Tech. To us, technologies that help companies meet regulatory requirements can be appealing for investment. An example would be something like methane monitoring and mitigation. To the extent a government decides that an area like methane should be regulated for environmental or safety reasons, there of course could be attractive investment opportunities in that area.

Examples of “climate tech” that we remain broadly skeptical of include so-called “green” hydrogen and sustainable aviation fuels (SAF). While exceptions always exist, the idea that either of these areas are anywhere near ready to scale commercially is ludicrous. One only needs to go back 2-4 years and those areas were featured in industry conferences as representing interesting growth opportunities.

Technologies that we think have inappropriately at times been labeled as climate solutions include EVs and solar + storage. Both sectors, in our view, are worthy of rebrands as Energy Tech. We expect both to experience significant growth in coming decades to help meet the massive unmet energy needs of the other seven billion people on Earth and to improve energy resilience and competitiveness amongst Lucky 1 Billion nations.

Energy Tech and Sector Convergence

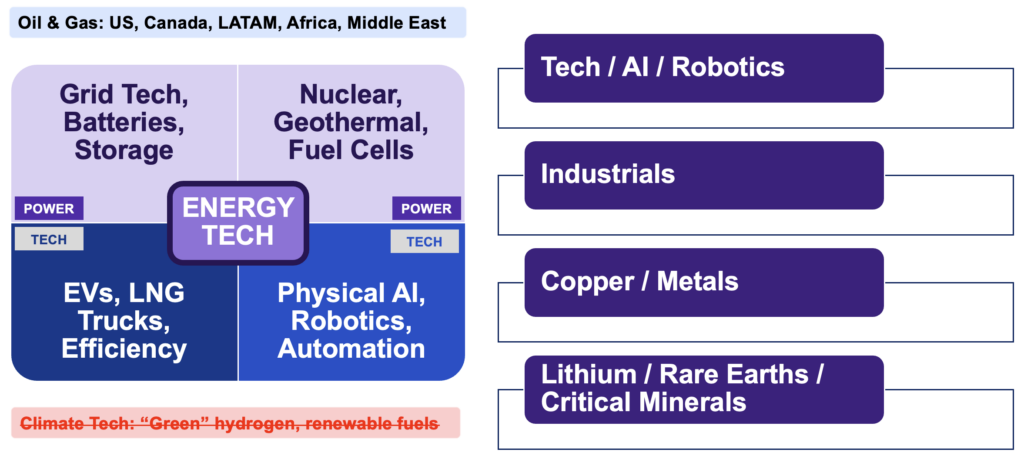

Exhibit 1 shows some of the major technology areas we are watching, bucketed into four different areas:

- Grid optimization: Grid Tech, Batteries, Storage, VPPs, DERs, etc.

- Power generation: Advanced nuclear, enhanced geothermal, fuel cells

- Diversification: EVs, LNG trucks, efficiency

- Manufacturing competitiveness: Physical AI, robotics, automation

Exhibit 1: Energy Tech & Sector Convergence

Source: Veriten.

Key questions that we would like to dig into or better understand in 2026 for each of these areas include the following:

Grid optimization: In particular in developed regions like the U.S. and Western Europe, what is the degree to which grid optimization solutions reduce the need for new power generation? To be clear, we will need new power generation. We are simply asking how much new power generation will be needed relative to grid tech opportunities.

New power generation: What are the proof points we will see in 2026 and into 2027 that can prove (or not) the potential for advanced nuclear, enhanced geothermal, and fuel cells to be a material component of power markets as opposed to a small niche (or not at all)?

EVs: Can any country compete with China? Will every other country on Earth simply accept the “Chinafication” of their auto industry? How does China compare to historic growth from Japanese and South Korean auto makers in prior decades? Similar risk? Worse? Not as bad?

Physical AI / robotics / automation: (1) Which companies can show a step change in growth and returns from applied AI? (2) What are the implications for energy demand from growth in this area? Additive or subtractive? Change in underlying energy sources needed? (3) What are the geopolitical implications from advancements in this area? If China is currently manufacturer to the world, does it have a huge leg up in this area already? Can advancements from US companies help the U.S. leapfrog or at least narrow the manufacturing gap with China?

An Update on Hyperscaler Profitability

One of the major debates in markets broadly and within the energy sector has been the major ramp in capital spending from the tech behemoths and the degree to which it will weaken profitability. Especially for those of us that have spent a career studying deeply cyclical, capital-intensive sectors like energy or metals and mining, we all know massive jumps in capital spending usually end poorly. We have written extensively about our Quadrilateral of Death framework for traditional energy CAPEX versus profitability (most recently here) that observed that as capital spending jumped during 2004-2014, profitability fell off a cliff despite dramatic increases in underlying oil prices.

It must be true that Big Tech will follow the same fate, no?

With all the caveats that our preference is to stay in our lane as energy experts—we have no background professionally covering the technology sector—we are going to offer some comments on how growth and returns are progressing for what we call the Hyperscaler-5 which are Amazon, Google, Meta, Microsoft, and Oracle.

Several framing points:

- We do not think a “quadrilateral of death”-like framework that is applicable to deeply cyclical, mature sectors like oil & gas or metals and mining will apply to technology.

- With technology, unlike say crude oil or copper, missing the next technology wave can be existential. It may not quite be zero or one, but legacy technologies do experience massive declines when the next big thing comes along.

- We would contrast technology cycles with traditional energy and raw materials that generally grow by low-single digit percentages over centuries with no end in sight. The inelastic and slow moving nature of both demand and supply invite boom/bust commodity and profitability cycles that are the core to investment analysis and corporate strategies.

- With technology, you either pivot to, participate in, and ideally dominate the new trend or you die a slow or quick death. Kodak is a classic example that some leaders recently mis-applied to energy.

Exhibits 2-5 analyze how we think the Hyperscaler-5 are doing in the midst of a major CAPEX ramp. Our key takeaway is that we lean constructive that the spending in aggregate is driving faster revenue growth and better incremental profitability than feared. We therefore expect the spending to continue. Key highlights:

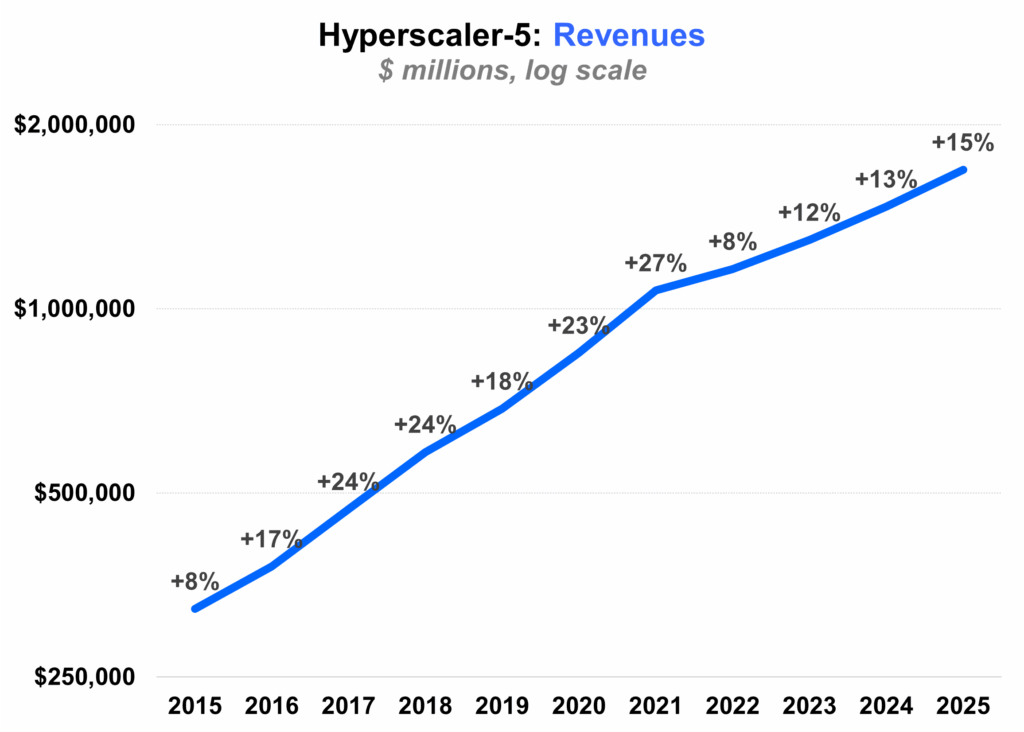

- Revenue growth from the Hyperscaler-5 has accelerated in each of the last 3 years after a sharp post-COVID slowdown in 2022 (Exhibit 2). Notably, the acceleration has occurred at the same time as the post ChatGPT AI awakening.

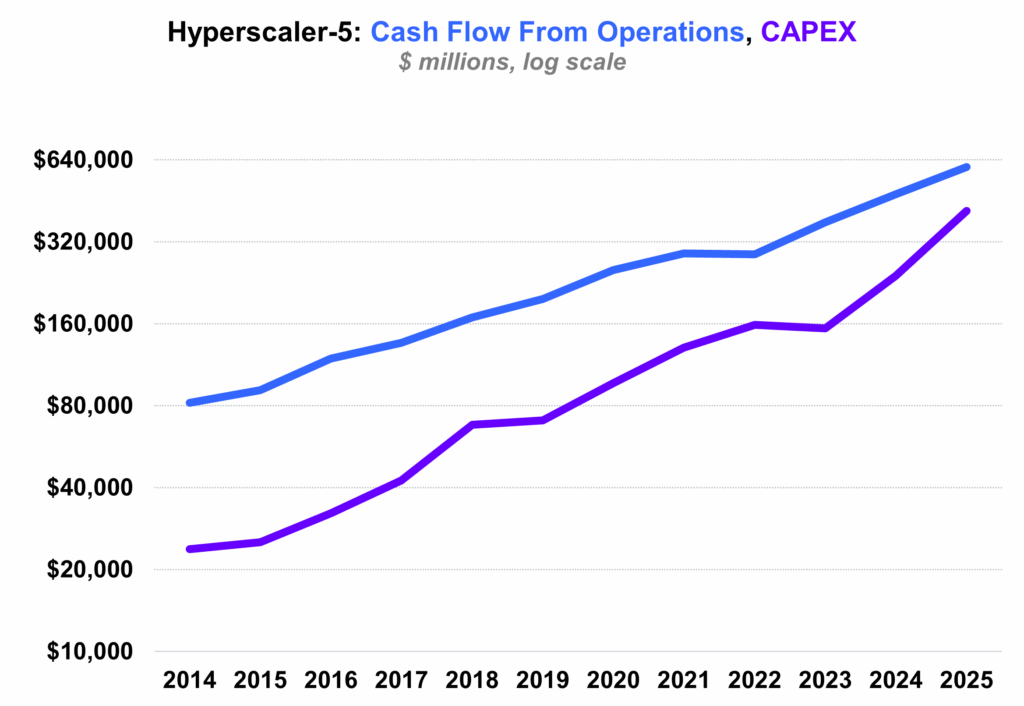

- Both CAPEX and cash flow from operations (CFFO) have ramped significantly (Exhibit 3). CAPEX is leading CFFO as would be expected. We will of course watch closely to see if the latest jump in CAPEX in 2025 and 2026 drives higher CFFO or not.

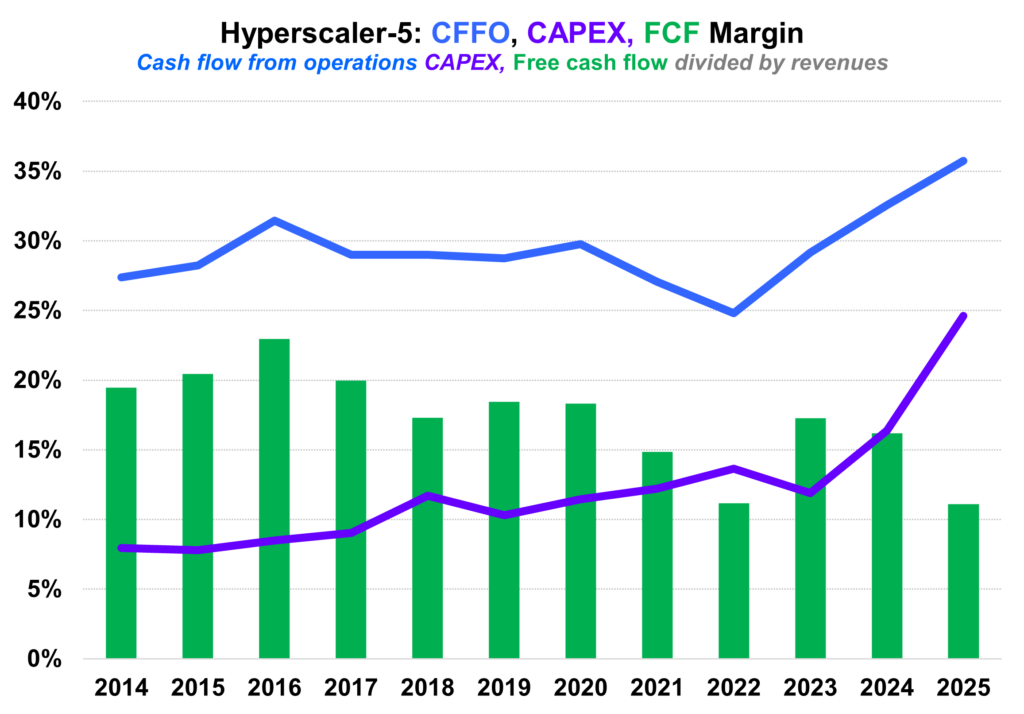

- In addition to the acceleration in revenue growth, we note that CFFO margins (relative to revenues) have also increased over 2022-2025 and are now at all-time highs relative to the past decade (Exhibit 4). In 2023 and 2024, free cash flow margins (the green bars) had improved, but ticked back down in 2025 on the latest jump in CAPEX.

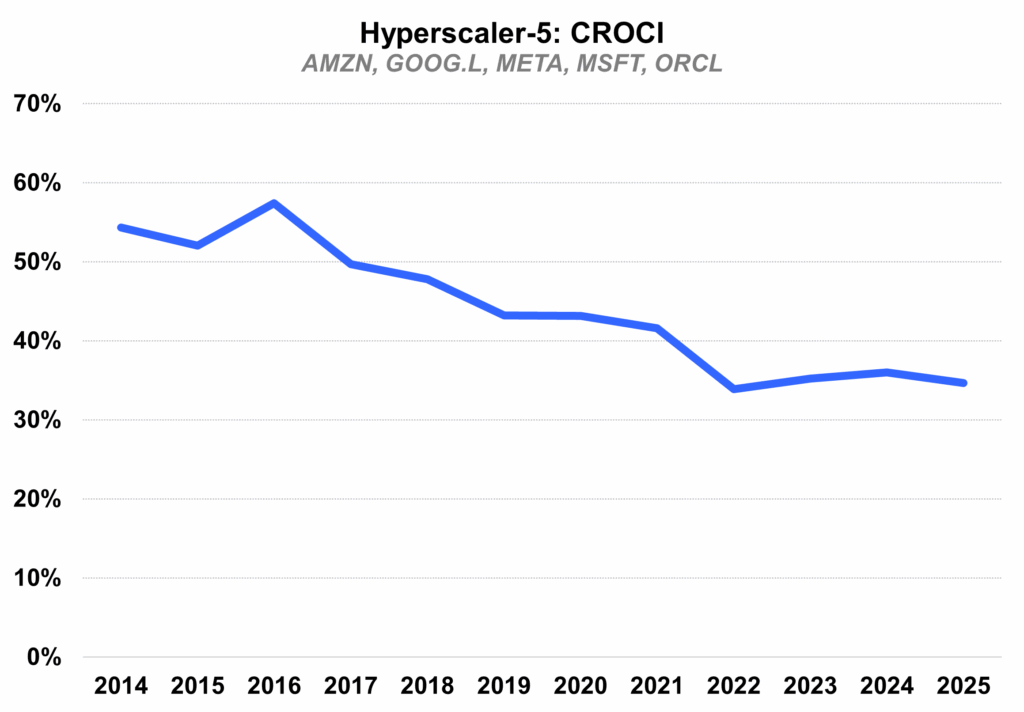

- Finally, and the ultimate test, CROCI (cash return on gross capital invested) has fallen over the past decade, consistent with rising capital intensity (Exhibit 5).

So does the fall in CROCI prove that the Hyperscaler-5 are no different than Big Oil or mining giants that overspent in past super-cycles only to suffer during the bust?

- Our instinct is that the dynamics that drive analysis of traditional energy and metals and mining are less applicable here.

- We find it of interest that CROCI has stabilized in 2023-2025 at a still incredible mid-30s%.

- There are differences amongst these companies that we do not plan on commenting on in Super-Spiked, as we are not professional technology sector analysts by background. In addition, we do not discuss contemporary individual companies in Super-Spiked.

- It is entirely possible that the latest jump in CAPEX in 2025 and 2026 will be unsuccessful; we will continue to examine profitability trends for these companies.

- That said, we are seeing a major shift toward the industrial application of AI from its consumer tech origin (e.g., ChatGPT) that gives optimism industrial and enterprise AI will be a major growth area.

Important cautionary notes on our analysis:

- Unliked traditional energy, we have no professional history of covering the technology sector.

- We are relying on FactSet-downloaded data and have not created our own company models for the Hyperscaler-5.

- It is possible there are company-specific adjustments to CFFO and GCI (gross capital invested) that are required that we have not made that could impact the conclusions we have drawn.

Exhibit 2: Hyperscaler-5 Revenues

Source: FactSet, Veriten.

Exhibit 3: Hyperscaler-5 Cash flow from operations and CAPEX

Source: FactSet, Veriten.

Exhibit 4: Hyperscaler-5 CFFO, CAPEX, and free cash flow margins

Source: FactSet, Veriten.

Exhibit 5: Hyperscaler-5 CROCI

Source: FactSet, Veriten.

Aramco, An AI and technology leader

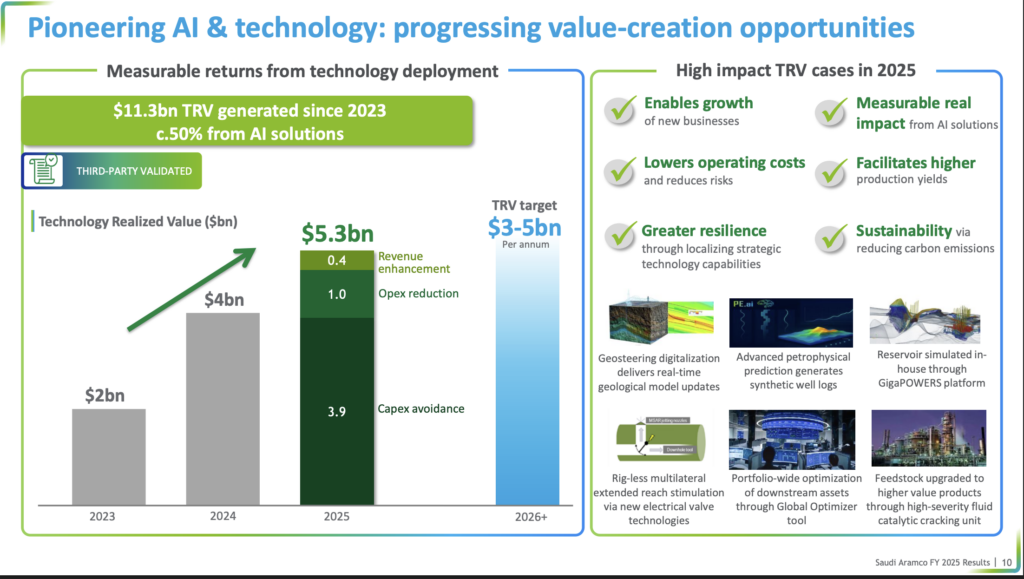

If you listen to or read quarterly earnings season transcripts in energy, power, and other traditional sectors, the topics of technology and AI spending will repeatedly come up. Credit to the Aramco leadership for providing the slide shown in Exhibit 6, which looks to quantify the value of its technology investments.

What a great title: “Measurable returns from technology deployment.” We find it striking that the figures provided are annual as opposed to cumulative. We appreciate Aramco has provided a target of $3-$5 billion per year for 2026+.

If other energy or power companies have provided a similar slide(s), please let us know in the comments section. This is a best practice, even as we would like to better understand the underlying the details for the breakdown and totals provided.

Exhibit 6: Aramco estimated value creation from technology

Source: Aramco

⚡️ On a Personal Note: Engaging with legacy media

As many of you have noticed, my interactions with legacy media (i.e., TV, newspapers) has increased meaningfully since early March. Some of that is of course simply a sign of the times with the War in Iran and higher oil prices increasing demand for energy expertise. But it also represents a change in heart on my part on the merits of engaging in the first place.

During my time at Goldman Sachs, the message from the top which filtered down to an equity research analyst like myself was to “just say no” when it comes to media engagement. I believe I conducted just three external interviews over the 2004-2014 super-cycle. I’ll do a separate write-up on Lloyd Blankfein’s great memoir, “Streetwise: Getting to and Through Goldman Sachs” (here) that I just finished reading. But Lloyd noted that when public sentiment turned against the firm in 2009 and 2010 after it successfully navigated the financial crisis (thanks to Lloyd’s leadership during those years), there was a reputational price to be paid for the historic reticence to interact with anyone other than our top clients, leading policy makers, and the elite of the elite.

As I’ve noted in Super-Spiked, there is a need for oil & gas leaders to speak up publicly using normal human language about their business and the critical importance of getting energy narratives and policy right. It is among the reasons I started this publication. In the modern age, one can go directly “to the people” via YouTube, LinkedIn, X (Twitter), and numerous other new media channels. Some of those channels have views and viewership that are many multiples of the reach of a TV show or news article.

That fact notwithstanding, I’ve changed my mind on the merits of engaging with legacy media. There is a need for it. The reach and audience is different. It is often broader and less deep, but that’s the point and the opportunity. The fact that we can all now live in a narrow, deep, self-selected information bubble has downsides. Legacy media is an offset to that.

X is a great place to get news first and to hear a broad range of global voices. I have made friends with X and find it to be a great resource. But I still double check to see whether Bloomberg, The Wall Street Journal, the New York Times, or The New York Post have confirmed that same news. Then I know its official. There is still very much a stamp of validity that comes from those organizations.

At Goldman, my focus was on servicing our leading investor clients. Full stop. Nothing, least of all personal publicity, would get in the way of serving those clients as best as I could. I hold that same philosophy with Veriten clients. But part of our mission at Veriten is, as the name denotes, spreading the mission of “Truth in Energy.” It is to push back on the ill-informed, partisan, ideological camps American energy narratives have devolved into. Engaging with legacy media is part of that mission.