As the Strait of Hormuz (SoH) Crisis completes its third month and on-again/off-again peace talks drag on, we are starting to see the outlines of various structural themes emerging, and, as importantly, some that are not. Thematically we see the following:

- Power Surge! Our Power Surge! super-cycle theme has not only not been knocked off track by the SoH Crisis, but has likely been enhanced based on “the four Ds” of pragmatic energy policy orientation we discuss below. Recently completed 1Q 2026 earnings season shows the AI (artificial intelligence) and broader digital transformation theme is as strong as ever.

- Geopolitical Super Vol. Geopolitical Super Vol remains our commodity macro framework, in particular for crude oil prices. Since Russia-Ukraine and through SoH-to-date, we have resisted crude oil super-cycle framings while also, importantly, rejecting perma bear doom-and-gloom. The unforgiving math of global oil demand being forced down to circa 95 million b/d of supply from around 105 million b/d pre-crisis suggests recession is the most likely clearing mechanism rather than a structural increase in long-dated oil prices in the event a significant disruption to flows persists. To be clear, we do see scope for a modest increase in long-end oil on the order of $10/bbl to account for both cost inflation and an increased geopolitical risk premium.

- Molecules to markets. In our view, getting molecules to markets is the more pressing strategic imperative for countries than simply trying to find the molecules in the first place. In traditional energy, this puts a premium on well-positioned midstream and downstream assets. In the upstream business, there is always an opportunity to find acreage that is well positioned on the future cost curve. Having a midstream or downstream solution (e.g., LNG) may be an increasing success factor for larger E&P (exploration and production) companies.

- New business models > pure-play (for larger companies). The era of extreme pure-play specialization we think will fade, or at least will no longer be the dominant ask of investors. Business model evolution is likely to continue to separate leaders from laggards. Examples we find intriguing include pressure pumpers and midstream companies diversifying into behind-the-meter (BTM) power, US shale gas producers expanding into midstream and potentially LNG, refiners that have grown midstream capabilities, midstream companies that have grown export opportunities, and the expanded commercial trading opportunities that larger companies have pursued. The list is growing.

- Brownfield > greenfield (usually). The advantage of doing more from existing assets is something both countries and companies have in common. Brownfield almost always beats greenfield on profitability and speed-to-market, though a best-in-class greenfield project like Guyana oil is the type of exception that exists to the general rule.

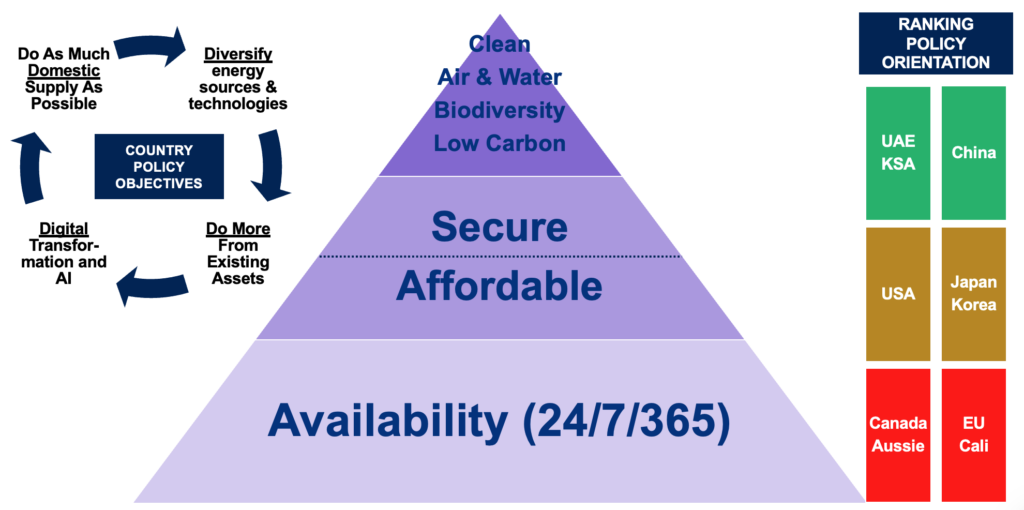

From an energy policy perspective, the Strait of Hormuz Crisis reveals what we are now calling the four Ds of country-level energy policy aspiration:

(1) Do as much Domestic production as possible;

(2) Diversify energy sources and technologies;

(3) Do more from existing assets; and

(4) embrace Digital transformation and AI.

The Four Ds of Pragmatic Energy Policy

The four Ds are the pragmatic policy implication of country leaders recognizing energy’s natural hierarchy of needs (Exhibit 1). On the right side of Exhibit 1, we rank (higher on list is better) resource rich countries and resource challenged areas in terms of federal policy orientation that recognizes energy’s natural hierarchy and implementation of the four Ds relative to a given country’s strengths and weaknesses.

Saudi Arabia and United Arab Emirates among resource rich regions and China among resource challenged areas we see as having favorable federal energy policy orientations. Laggards are not surprising: Western Europe, California, Canada, and Australia. What KSA, UAE, and China have in common are national leadership that emphasizes the ideas of “all of the above,” maximum (or optimal) output of what you can control, and unapologetic “their own country first” mentalities.

Super-Spiked subscribers know we have a very favorable view of Canada’s oil and gas potential and the leading companies in the province of Alberta. We had an unfavorable view of the federal energy policies pursued by the prior Trudeau regime, with the jury out on the current Carney administration. On the latter, we appreciate that the rhetoric has improved off a low starting point. The proof will be in the policy implementation pudding.

No country should aspire to follow the path of California or Western Europe and their “climate first” ideology (dishonorable mention goes to many states in the US northeast). Sadly, poor energy policy choices made in those areas are going to mean that less fortunate consumers and businesses in developing Asia suffer from being outbid for needed energy like LNG, jet fuel, and diesel during times of stress, as we last saw in the early days of Russia-Ukraine. It has been some time since we have done a deep dive on Australia; our sense would be that it is in the Canada category of having substantial oil and gas resources that the world would massively benefit from, but is being held back by ill-advised climate-first ideology by its national leaders.

Exhibit 1: A Hierarchy of Energy Needs & Country Policy Objectives and Orientation

Source: Veriten.

Doing More From Existing Assets

In previous issues of Super-Spiked, we have discussed three of the Ds: do as much domestic production as possible, diversify energy sources and technology, and embrace digital transformation and AI. Therefore, in this post we will expand on the “do more from existing assets” theme.

- A major advantage the developed world has over China, India, and other developing areas is a large installed base of assets and infrastructure. Prematurely retiring old power plants in the name of “energy transition” and “The Climate Crisis” is the type of 2020-2023 mistake that has hurt competitiveness and affordability in the United States and Western Europe. In power generation, we are intrigued with trying to answer the question of how much new generation from legacy sources (e.g., natural gas, BTM, and traditional nuclear) is needed versus how much new generation technology is needed (e.g., fuel cells, enhanced geothermal, advanced nuclear) versus how much can existing grid utilization be improved via flexible loads and various grid enhancing technologies. How much more can we get from existing is important to how much we need from the other two options.

- In crude oil markets, we do not believe there is the urgency to figure out “what’s next” from a resource perspective as there was in the 2004-2014 super-cycle. To be clear, this comment is intended at the macro level; individual companies are almost always in need of figuring out what’s next. Exploration and capital spending is likely to grow but we do not believe the kind of re-rating that happened during China/BRICs is warranted now. Rather we are most intrigued with what companies are doing to extend asset life (i.e., resource to production ratio) via a combination of technology application, business development, and midstream/downstream investment that can ensure molecules get moved to markets and turned into usable end products. Ironically, the Middle East looks like a compelling upstream opportunity for western oil and gas firms, given improved fiscal terms in certain areas. We have long held a favorable view of Canada (our concerns about its federal energy policies notwithstanding) and Alaska. Recent developments in many Latin American countries warrant a fresh look at the region for western players.

- The largest areas that seem ripe to “do more from existing” include US shale oil, US shale gas, Middle East oil, Canada’s oil sands, Venezuela oil, and developed market power grids.

Growth and opportunity

The five areas of energy where we are most confident in growth include:

(1) US and global power generation

(2) Midstream and downstream infrastructure for crude oil and various metals and minerals

(3) Grid enhancing technologies

(4) US and global natural gas

(5) Renewables and storage

The long-term opportunity to grow nuclear power is going to prove to be compelling for many countries, justifying the required patience in terms of time to development. Nuclear is the ultimate baseload, domestic, clean energy source.

We remain open-minded about emerging and new energy technologies. We are seeing current growth in fuel cells and optimism about enhanced geothermal on the power generation side of the business. The SoH Crisis will accelerate adoption of electric vehicles and LNG trucks in particular in oil importing countries for diversification and affordability reasons.

The success of new business models should diminish investor and activist demand for pure-plays

There is a misperception that investors prefer pure-plays or that investors only want more dividends and stock buybacks. Investors prefer companies that generate superior profitability with differentiated growth. Both are needed to sustainably outperform: profitability AND growth.

The challenge in mature, cyclical sectors is that corporate over-enthusiasm for growth usually erodes profitability to the point where investors demand a disavowal of growth in favor of profitability and returning capital to shareholders. To be sure, if structural demand growth for a given commodity is something like 1%-2% per year, the expected growth rates for the largest companies within that sector is unlikely to be any more than +/- 1%-2% of the broader demand trajectory.

As businesses mature and growth slows, the demand by investors to focus on sub-parts of the business often increases in order to enhance the combination of per share growth and profitability for a particular business segment. The post-2014 oil super-cycle bust and growth in U.S. shale turbocharged the demand for pure-plays, especially within the traditional oil & gas value chains. Certain pure-play shale oil producers, midstream companies, and refiners in fact performed exceptionally well.

Power is clearly in a super-cycle and traditional oil and gas is operating with a Geopolitical Super Vol macro backdrop (a dramatic improvement from the post super-cycle bust phase of 2015-2020) and business opportunities abounding in the different product lines and geographies.

SoH Crisis FAQ

Question 1: Has an oil super-cycle begun?

Answer: No. Our core view remains Geopolitical Super Vol, not super-cycle.

Q2: Have the odds of “peak oil demand” increased?

A: No, we don’t think so. However, we are concerned that if the Strait remains significantly disrupted that the painful adjustment down in global oil demand could mean that we spend a good part of the remainder of this decade recovering back to pre-crisis demand levels as incremental supply is brought online. In our view, the timing of a more permanent peak in oil demand is unknowable so long as the other seven billion people on Earth continue to use only a fraction of the energy The Lucky 1 Billion of Us take for granted.

Q3: Isn’t AI and the resulting power demand growth forecasts a bubble waiting to pop?

A: No or, perhaps more accurately, not at this time. The fact that numerous stock markets like the U.S. (S&P 500), Japan (NIKKEI), and South Korea (KOSPI) are at or near all-time highs may indeed reflect complacency with the risk of global recession due to the ongoing SoH Crisis. We would differentiate stock market complacency with an AI bubble. We see it in the areas where we spend a lot of time: digital transformation and the application of AI is a game changer for numerous businesses. The stock market may well experience a major correction if the world tips into recession. Whatever short-term setback that might mean for near-term power generation we think would be akin to the Great Financial Crisis hit to oil demand in the middle of the China/BRICs super-cycle of 2004-2014, i.e., it was temporary.

Q4: Don’t investors prefer “pure-plays” over diversified companies?

A: That view is missing our point. Investors prefer companies with competitive profitability and differentiated growth opportunities. The demand for “pure-plays” typically is the result of a mature sector experiencing a structural downcycle and investors being disappointed on both profitability and growth. And for sure, some companies should remain as pure-plays. The larger a company’s market capitalization and overall size, the less we think a pure-play business model makes sense, be it basin or geography or asset type or business line. For small-caps and new technologies, the pure-play business model is often logical.

Q5: So E&Ps will merge with refiners?

A: No, we aren’t expecting that type of integration or diversification. A future “integrated E&P” likely means some combination of midstream and commercial exposure as opposed to a historical upstream-refining mix, as an example.

⚡️ On a Personal Note: Work Hard. Golf Hard.

It’s been a great three-week stretch of Spring golf ramp-up. 8 rounds in 5 days in and around Troon, Scotland the first week of May and then our NJ club’s flagship member-member Governor’s Trophy tournament over Memorial Day weekend featuring 45 holes of match play over 2 days. Day 2 of Governor’s featured a good Scottish cold snap of low 50s weather and a light drizzle. Glad my rain pants got more work in and happy to be in sunny Houston as I finish writing this.

At Governor’s you can always see the short-game comfort from the returning Florida crowd versus those that stayed north over what is typically a 4-5 month winter hiatus. I failed to take advantage of part-time Houston residency this past winter and my partner and I didn’t win our flight for the first time since 2021. Five 3 puts—FIVE!!!—from yours truly in Round 2 and two more missed make-able putts in Round 3 were seven half-point giveaways we did not overcome. Based on my accounting, my partner cost us only 2 points versus my 7.5, so the disappointing performance is on me. I’ll need a stricter winter routine next year.

I will say the Scotland golf intensity helped stamina at Governor’s. The intensity and deliberate pace of hole-by-hole match play is usually mentally and physically draining. I didn’t feel that this year. For future reference: I need to play 36 more often! It forces an easier swing. It improves mental resilience. Seems better than a cold plunge.

Does a high level of golf intensity make you a better energy equity analyst, advisor, or board member? For sure it does. There is no question about this. Are we advising our companies to settle for mediocrity? That an 8% return on capital is good enough? That sector average TSR is fine? Of course not.

Work Hard. Golf Hard.

A Lot of Great Golf In Scotland: Western Gailes Near The Top Of My List

Source: Super-Spiked selfie.

The Calm Before The Governor’s Trophy Storm

Source: Super-Spiked.