This week we return to a Q&A styled note to address implications of the surprise OPEC cut from last Sunday. As always, our ultimate focus is on how this event impacts our intermediate- and longer-term views.

Do OPEC cuts mean there is no longer any reason to worry about a future deepening of the banking crisis or global recession?

Absolutely not. A banking (or any other economic) crisis will always win if it means a hard landing is coming. In a soft/no landing scenario, the cuts have more relevance to supporting/boosting prices.

Has OPEC raised the floor price for oil?

Yes, for now, but see previous point. Deep recessions are bad and would almost certainly overwhelm OPEC’s ability or willingness to defend a $70/bbl or $80/bbl floor. However, in the soft or no landing scenario, the odds of a sub-$60 oil price in the next 12 months seem far less likely.

Have the odds increased of a return to $100+ in 2H2023 or 2024?

Aside from again repeating the hard vs soft landing commentary, the other question is the degree to which these “cuts” are really masking underlying production issues with various countries. Geopolitical turmoil remains high. The world is not well protected should unexpected downtime occur in any number of important and perhaps even less important producers. It remains our view that true flexibility within OPEC countries is mostly limited to Saudi Arabia and United Arab Emirates.

Is this an example of OPEC gaining market clout due to a lack of CAPEX, etc.?

It’s too simplistic to say OPEC is in control of oil markets and we don’t agree with that conclusion. There are likely many reasons for the surprise cut. First, there is likely a desire to get ahead of potential demand weakness in the event a more meaningful economic slowdown materializes later this year. Clearly, there is a growing confidence within OPEC+ that a non-OPEC supply boom isn’t likely anytime soon and that the elasticity of US shale in particular to higher prices is more muted than in past years. Some OPEC members were likely upset that the US is not refilling its SPR. Finally, several OPEC+ members are possibly having their own production issues, meaning not all of this cut may be voluntary.

At a time of limited spare capacity, cyclically subdued CAPEX, generally low inventory levels, and diminished US shale price elasticity, OPEC is in a better position to support prices in a non-recessionary demand environment is about as far as we would suggest going. The “OPEC is back in control of oil markets” narrative overstates their actual ability to set oil prices. OPEC+ is one factor, not the factor.

Does this mean we are moving from a Super Vol macro backdrop to one of diminished volatility with OPEC modulating away the extremes?

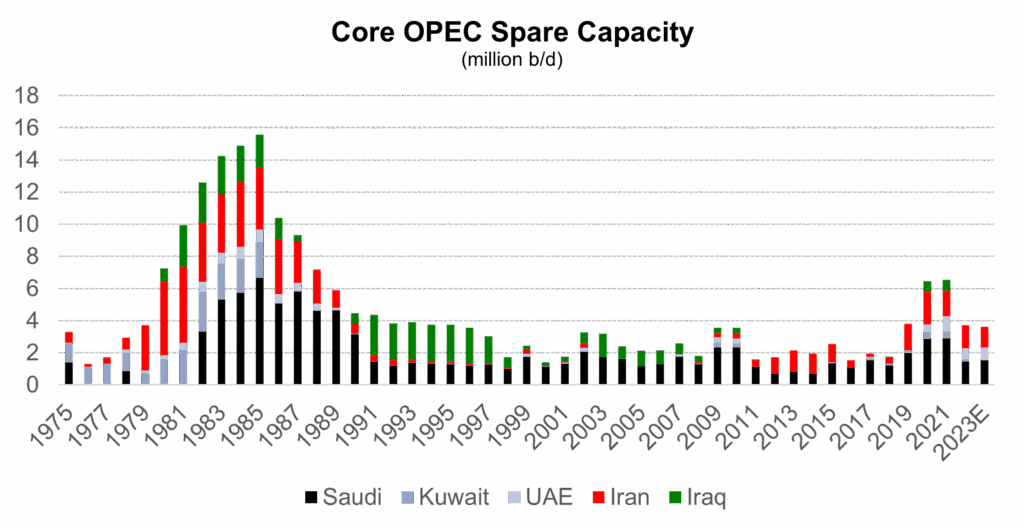

I seriously doubt it. The level of OPEC spare capacity remains modest (Exhibit 1), overall industry capital spending remains way below “danger zone” levels, non-recessionary demand remains much healthier than many perceive (i.e., we are no where near peak oil demand assuming trend global GDP growth), US shale growth is showing signs of maturing (albeit still expect to grow for next several years), and geopolitical turmoil remains high. There is no part of that which suggests a lower volatility environment is around the corner.

In my view, volatility is OPEC’s friend as it further disincentivizes non-OPEC capital formation. The very nature of such an unexpected cut calls into question the notion that this is somehow about volatility reduction.

Exhibit 1: OPEC spare capacity is a far cry from what it was in the 1980s

Source: BP Statistical Review of World Energy, IEA, Super-Spiked.

How should investors or companies adjust their outlook for traditional energy post the OPEC+ cuts?

For both investors and companies, trying to cycle time is difficult. Trying to time geopolitical turmoil and OPEC+ actions is even harder—not impossible, but harder. On the geopolitical turmoil part which might sound like it would be impossible to trade, there are periods of relative calm and relative intensity. The instinct many times should be to go in the opposite direction of prompt relative tension. That said, we do not seem to be at an extreme either on the downside or upside in terms of price, valuation, or any other metric at this moment. That makes it more difficult to say in the short run “you must buy” or “sell” or do anything else.

For investors, it remains my view that when you add up the mini-peaks and troughs along the way, overall profitability and cash returned to investors for top quartile and possibly the top two quartiles of traditional energy, it will compare very favorably with the broader S&P 500 over the coming decade. Hence, my personal approach is a “buy, hold, and possibly trade around the edges” approach to traditional energy. I have never been a short-term trader; others that are can have at it.

For companies, a fortress balance sheet protects against downside volatility as well as the risk that banks and insurance companies may increasingly go away as major sources of financing/support for traditional energy. This is clearly on-track in Europe; we can only hope sanity ultimately prevails in the United States. But hope is not a strategy. There is nothing about this surprise OPEC cut that suddenly suggests an impenetrably higher oil price floor has arrived.

If oil markets are so tight and suffering from underinvestment, why are long-dated futures prices not higher?

This has become one of my favorite recent questions. Comments are often made that forward prices are not signaling that oil markets are tight. As we wrote about (here), forward prices should not be used as a prediction of where prices will be in the future. They are merely today’s reflection of future prices. Tomorrow’s reflection of futures prices may move higher or lower based on updated information.

Right now, markets embed a view that oil demand is at or near its ultimate, permanent peak. We do not agree with that view. If that view is revised up and CAPEX remains subdued, we would expect forward prices to move higher, all else equal. The opposite would be true if it turns out that not only are we at peak oil demand but that the future downward slope is sharper than what is currently forecast. These are but two examples for why forward prices may change up or down in the future. We remain in the camp that oil demand will structurally increase into the 2030s. There is no guarantee we will be correct.

An alternative explanation for today’s forward price level could be that the market actually expects a “Super Vol” spot environment that will knock out demand when spot prices spike and will either knock out supply or stimulate demand when spot prices fall, which would ultimately net out to the type of forward prices currently seen. I would not rule out this explanation and would again guard against an assumption that spot volatility will necessarily be low simply because back-end oil hasn’t moved as much as a tight market might otherwise imply.

Without CAPEX and sufficient supply growth, demand will be forced to contract at times. In my view this is a particularly unhealthy way to keep oil markets in balance given how challenging so-called demand destruction planning is for citizens around the world.

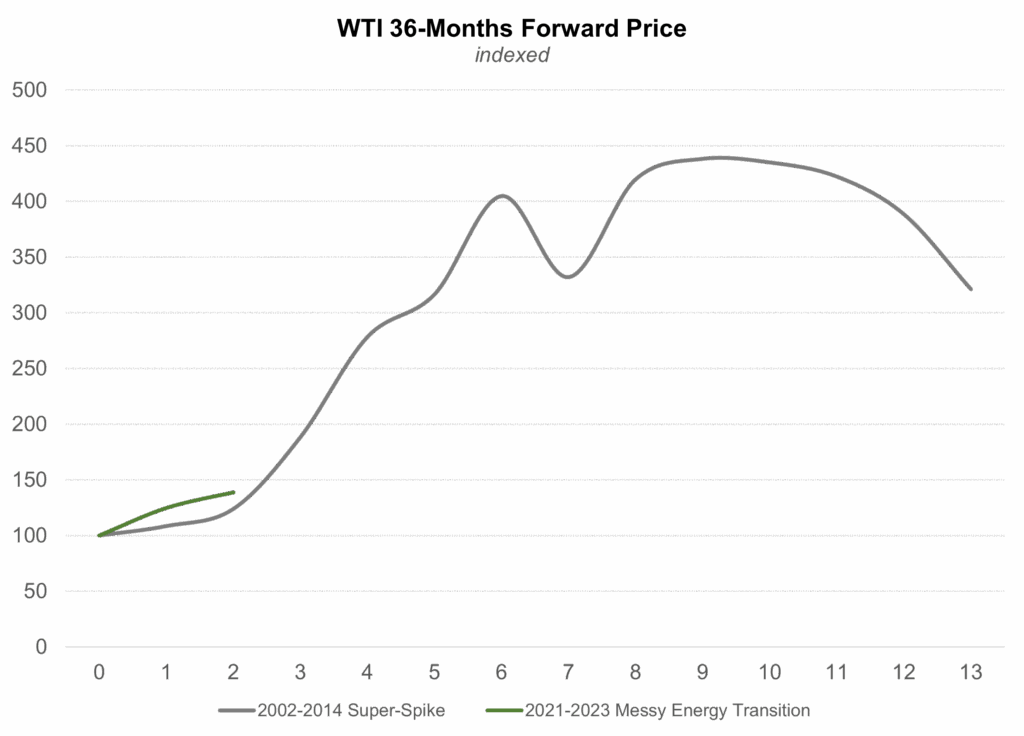

How does the forward curve progression compare with the prior Super-Spike era?

It is surprisingly similar at a similar point in time. Exhibits 2 and 3 show the year-end 36-months forward price for WTI crude oil over 2002-2014 versus 2021-present using absolute prices and then indexed to 100 to adjust for the absolute value differences. Exhibit 3 shows that in the first year of both periods, long-dated prices rallied about 20%.

In the prior Super-Spike era, long-dated WTI continued to rally as non-OECD oil demand surged despite higher oil prices. This time around, the fundamental economic backdrop is not as healthy, at least not at this moment. However, the CAPEX outlook is also less optimistic than last cycle, suggesting there may well be considerable upside risk to long-dated prices as or if market participants recognize oil demand has not peaked and is not rolling over any time soon (ex-recessions).

Exhibit 2: WTI 36 months forward price: A comparison of the Super-Spike era versus the current Super Vol period

Source: Bloomberg, Super-Spiked.

Exhibit 3: WTI 36 months forward price comparison of then versus now using indexed values

Source: Bloomberg, Super-Spiked.

🎤 Streams of the Week

Highlighting a healthy, pragmatic discussion with my friend and colleague Jason Bordoff, founding director of the Center on Global Energy Policy. I have benefited immensely from my involvement with CGEP, where I am an advisory board member, and the diverse viewpoints and debates we engage in as a team. At a time when so many stay in their ideological echo chambers, I appreciate being challenged about my views and having the opportunity to challenge back. CGEP is global and it is non-partisan.

Jason I know doesn’t agree with every perspective I provide and vice versa. The point isn’t to have kumbaya agreement or conversely to shout down counter viewpoints. It is to understand the differences and to figure out how our own views can be tweaked or even changed accordingly. I am grateful for all that I have learned in being part of the CGEP team.

Link (also on Apple Podcasts): Wall Street’s Role in the Energy Transition – Center on Global Energy Policy at Columbia University | SIPA

⚡️ On a Personal Note: ‘Stros

The un-retirement honeymoon is over. Our first Veri-conflict. It’s baseball season. Veriten is Houston based. I somehow didn’t put 1 and 1 together to recognize that the Astros would be the default Veri-team. This is going to be a problem for a lifelong Yankees fan. As a new employee and in deference to my otherwise wonderful colleagues, let me offer the Top 10 most positive things I can say about Houston’s major league baseball team:

- George H.W. Bush was an Astros fan. He is the first president I voted for in the first election I was eligible to vote. It was always great to see him in the stands behind home plate. It made watching the Astros tolerable.

- The late J.R. Richard was one of my favorite non-Yankees pitchers that I loved watching in the 1970s. I remember how upsetting it was when he suffered the stroke in 1980, nearly a year after Thurman Munson’s untimely passing.

- The Astrodome was the 8th wonder of the world in the 1970s.

- The 1970s era uniforms were some of the best of any team in any major sport.

- Some will agree with me that Andy Pettitte is easily the most likeable Astros player of all-time, the son of a Deer Park refinery worker (I believe), and someone the Yankees should never have let leave for his hometown team.

- There are many people on Earth who are worse human beings than Jose Altuve. Kim Jong Un. President Putin. Prince Andrew. All definitely worse than Altuve.

- Numerous baseball teams have had issues with cheating, so I don’t personally put an asterisk next to the 2017 Series. Houston won it as fair and square as existed in baseball in 2017. Case closed.

- Following a second World Series title in 2022, the Astros are quickly closing in on the 27 championships the Yankees have won…only 25 to go!

- Minute Maid Park should revert to its original name. Truth in Baseball Park Names should become a Veriten slogan.

- Having the Astros win is better than having the Red Sox win.

J.R. Richard, an all-time great and my favorite non-Yankees pitcher

Source: Astros Daily

In all seriousness, the Astros in recent years have arguably had the best front office in baseball, using a mixture of modern data analytics and disciplined investing to field a highly competitive team that has won two World Series titles. In oil & gas terms, best-in-class executive team using data and competitive advantage to successfully invest in promising talent that have developed into major assets. Management has then “sold” the asset (i.e., let go in free agency) and not paid up for unsustainable, peak performance. While the analogy may not fully hold, it’s akin to a top tier E&P that is constantly looking for the next great, low-cost resource, while selling out of a mature asset at peak optimism.

The Yankees of the past decade are perhaps analogous to the once storied Super Major that struggled to adapt first to the shale business and more recently to energy transition. Are the Yankees the ExxonMobil of baseball? The dominant franchise from 1910-2010. Peaked in 2009. Still “big” over the last decade, but no championships and diminished in relevance. Greatest sporting franchise in the history of the world, broadly and dare I say unfairly disliked by non-fans, but with clear potential to dominate once again. I can only hope so. Maybe my friends at EngineNo1 can help inject new life into the Steinbrenner family? Hal is no Lee Raymond George.

⚖️ Disclaimer

I certify that these are my personal, strongly held views at the time of this post. My views are my own and not attributable to any affiliation, past or present. This is not an investment newsletter and there is no financial advice explicitly or implicitly provided here. My views can and will change in the future as warranted by updated analyses and developments. Some of my comments are made in jest for entertainment purposes; I sincerely mean no offense to anyone that takes issue.