We continue our series on re-focusing energy discussion and debate to how to best meet the substantial energy needs of the other 7 billion people on Earth that are not among the lucky 1 billion of us that live in the USA, Canada, Western Europe, Japan, Australia, or New Zealand. The outlook for energy will be dominated for decades to come by four groupings of approximately 1.4 billion people—what we are now calling The 1.4 Billion People Club: China, India, Africa, and Southeast Asia (i.e., Asia excluding China, India, Japan, and the Middle East). All four members currently consume a fraction of the energy used in the fully developed world. Economic, social, and environmental justice for all requires a closing of that gap eventually and inevitably.

The 1.4 Billion People Club members are all at different stages of energy usage and economic development, with different priorities, objectives, and challenges for their next stage of growth.

- China: China is ending a 20-year period of massive progress and is now working through the growing pains as it transitions to a potentially very different economic model going forward. We see China’s ongoing transition as one of the key contributors to our “super vol” rather than “super cycle” commodity macro view at the present time.

- India: India is gaining in momentum, and we expect substantial growth in Indian energy demand in coming decades. That said, we think India’s economy will develop differently than China’s did, with relatively less emphasis on energy-intensive heavy industry, exports, and property market development. While ultimate energy demand will still be sizable, the pace of growth may be slower than what China exhibited over 2002-2014. A better comparison is likely the other countries in Southeast Asia, i.e., meaningful but steady energy demand growth over the long run.

- Southeast Asia: Southeast Asia (excluding China and India) includes some countries that are now relatively more advanced, with further economic and environmental progress the key goals. Others are at earlier stages of development similar to India.

- Africa: The 54 countries that comprise the continent of Africa are collectively still in a pre-growth phase. Africa’s key objective has to be to break free from European and western world institutions and influence and chart their own course forward. Incredibly, Africa as a continent exports more energy than it uses. The legacy reasons for this are what they are and beyond the scope of Super-Spiked. Going forward, there is a massive opportunity for Africa’s resource and mineral wealth to be directed inward rather than outward.

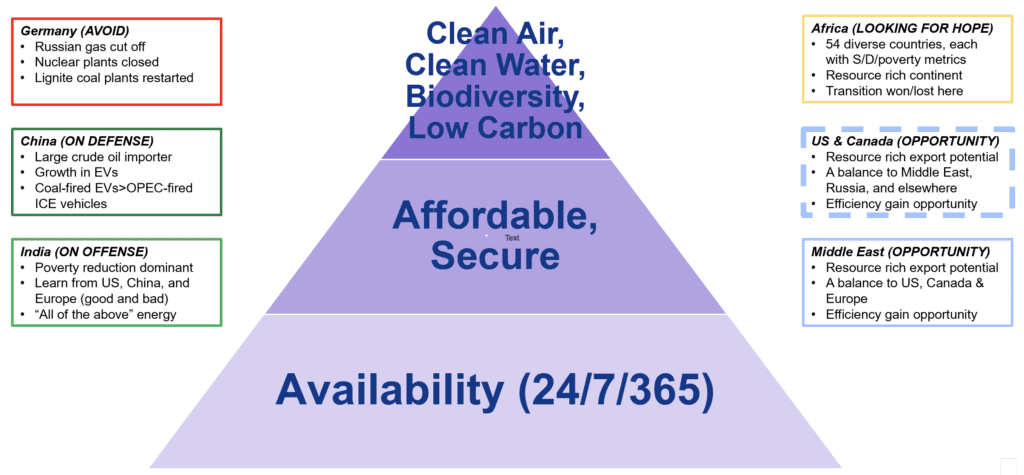

We have characterized energy priorities as meeting a hierarchy of needs (Exhibit 1):

- Energy will need to be available 24/7/365.

- Energy will need to be affordable to consumers that have a fraction of the disposable income seen in the rich world.

- Domestic sourced supply will be preferred over imported energy.

- Clean air, clean water, biodiversity, and carbon emissions are factors that will be taken into account as countries move up the income ladder.

It is important to note that we believe decarbonization and other environmental objectives go hand-in-hand with geopolitical security, and, if done right, reliability and affordability. If done wrong, none of the aforementioned objectives are likely to be met.

A final point that we did not include in our original hierarchy of needs is self-determination. In a multi-polar world, The 1.4 Billion People Club members will want to chart their own paths forward, independent of western world (especially European and American) interference, influence, and lecturing. We believe China and India are most capable of going it on their own, as are many of the other countries in Southeast Asia. It is the continent of Africa that has not yet achieved escape velocity. It does, however, enjoy a massive energy and minerals resource advantage over many other regions. The key is using that competitive advantage to further domestic economic gains.

Exhibit 1: A hierarchy of energy needs

Source: Veriten.

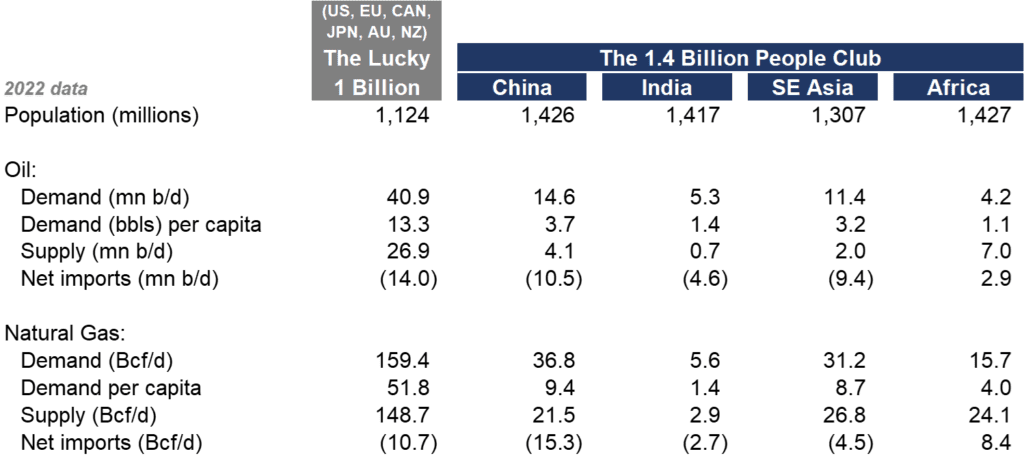

The Underlying Numbers

Exhibit 2 summarizes key statistics for oil (liquids) and natural gas demand, supply, net imports, and per capita demand figures for The 1.4 Billion People Club versus The Lucky 1 Billion. A few points to highlight:

- Per capita figures for oil and natural gas among The 1.4 Billion People Club are a fraction of The Lucky 1 Billion.

- Africa is somehow a net exporter of oil and natural gas despite having generally low levels of energy demand.

- China and Southeast Asia are decently ahead of India and Africa on economic progress and point to what is possible with the latter two regions.

Exhibit 2: Energy usage comparison: The Lucky 1 Billion versus The 1.4 Billion People Club

Source: EI Statistical Review of World Energy, IEA, Our World In Data, Veriten.

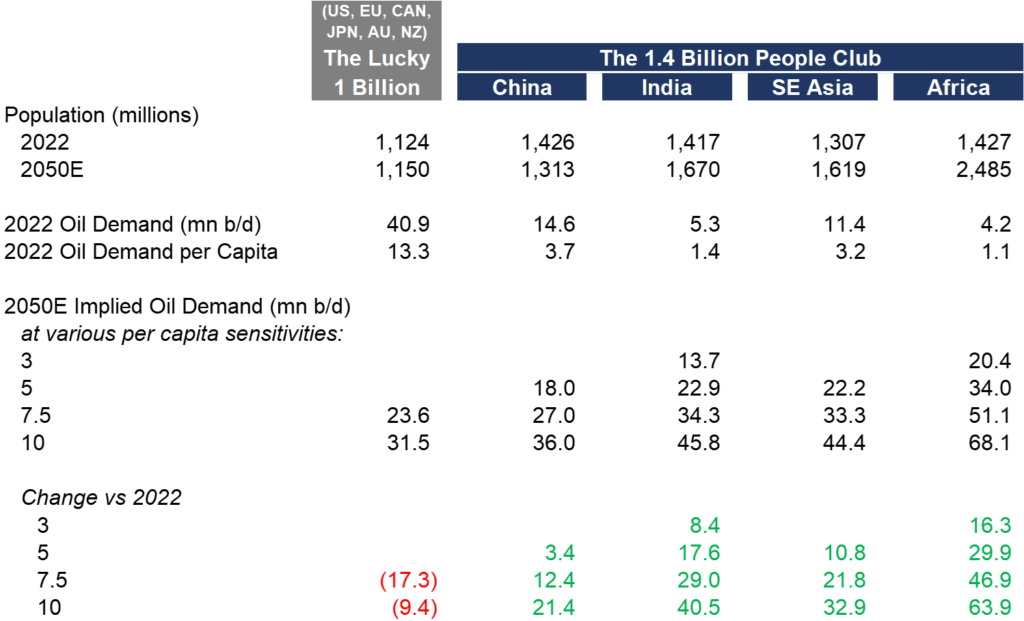

The Growth Potential

Exhibit 3 shows the kind of latent oil demand growth potential that exists on a global basis as the Rest of the World climbs the income ladder. A few points to clarify our views:

- The purpose of the table is to show indicative, order-of-magnitude oil demand potential by region. This is not a projection of actual oil demand for 2050 or any other year.

- The intent is to show the significant hurdles that exist with current “peak oil demand” arguments, given the wide variance between rich country oil demand and the significantly larger Rest of World population.

- In essence, the potential negative hit to rich country oil demand pales in comparison to the significant growth potential in the Rest of the World.

- We have used 2050 in this example, but we could just as well have used 2075, 2100 or any other year.

- Different regions will grow at different speeds and are subject to a host of risks and opportunities that could drive a wide range of economic growth and oil demand scenarios.

- That said, we believe there will be an inextricable march toward progress and lifting all people out of energy poverty.

Exhibit 3: Upside demand potential among The 1.4 Billion People Club swamps potential demand reductions from The Lucky 1 Billion

Source: EI Statistical Review of World Energy, IEA, Our World In Data, Veriten.

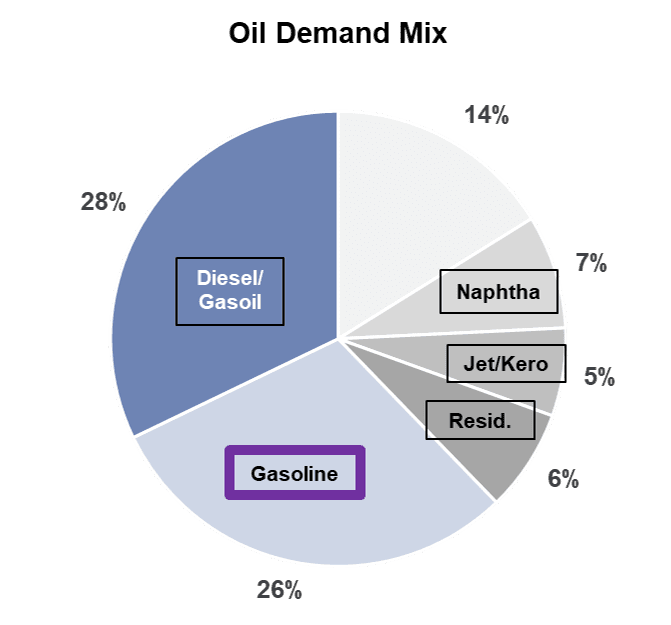

The Growth Challenge

Exhibit 4 shows the breakdown of global liquids demand by end use. Growth in consumer electric vehicles (EV) essentially address the gasoline wedge, or about one-quarter of oil demand. In the rich western world, it is not unreasonable to argue that over the next 25-50 years, the fleet of internal combustion engine (ICE) passenger vehicles could be substantially replaced with electric alternatives. This would address about 10 million b/d of the 41 million b/d of current rich country oil demand.

In the developing world, the numbers are staggering. The implied crude oil import needs of China, India, and Southeast Asia point to policies that will attempt to electrify as much of the passenger vehicle fleet as possible. That said, there is no EV free lunch when it comes to the similarly staggering implied growth and (effective) import dependence on critical minerals in the EV supply chain. Pick your poison. The lesson from countries like Japan that successfully went from poor-to-rich last century is that diversification of energy and critical minerals supply is the most sensible path.

India will not want to follow in China’s crude oil import path. That said, its eventual growth potential is so large and electric grid expansion has its own challenges that it appears inevitable that meaningful oil import increases will occur in coming decades, even if it is successful in growing EV sales. And there is of course still the other 75% wedge of oil demand that consumer EVs do not impact.

Exhibit 4: EV substation risk primarily applies only to about one-quarter of the demand barrel (liquids)

Source: IEA, Veriten.

Inevitable Long-Term Oil & Gas Demand Growth Is Distinct From Profitability and Price Cycles

A common misperception of our energy demand analysis is to conflate confidence in long-term oil and gas demand growth with a bullish or, worse, perma-bullish outlook for the sector or commodity price cycle. The business is cyclical: always has been and always will be. The cycles are inherently long-term in nature: 10-15 years up, 10-15 years down.

Demand, price, and profitability are all different issues. As we know, oil demand has grown nearly every year since the industry’s founding 150 years ago. Yet, we also know there have been many oil price and profitability cycles throughout history. It has been anything but a straight line up. Best-in-class traditional energy companies have transcended cyclicality.

In summary:

- We do not believe the oil and gas industry is anywhere near its sunset phase, not so long as there is such a massive gap between the energy needs of the other 7 billion people on Earth and the lucky 1 billion of us.

- The capital spending cycle will drive the timing and magnitude of the supply response to rising oil and gas demand; hence, price and profitability cycles are more driven by the timing of CAPEX vis-à-vis demand, rather than solely demand.

- Geopolitical volatility can have a meaningful and potentially multi-year impact on prices and profitability.

- Currently, we believe the CAPEX cycle is still closer to trough than even mid-cycle let alone peak, which bodes well for structural profitability in the context of this decade.

- We believe many industry observers are way too bearish on long-term oil demand, leading to a subdued CAPEX impulse.

⚡️ On a Personal Note: Metallica at MetLife

On August 4, I attended Metallica’s 72 Seasons tour at MetLife Stadium with two of my closest friends whom I’ve known since the 7th grade (junior high as it was then called). Metallica still has it musically, even if their most recent albums pale in comparison to their earlier offerings. While Metallica’s genre of metal has gained in popularity since their 1983 debut Kill ‘Em All, it was still pretty impressive to see 80,000 fans in attendance to watch a group that is in its 40th year of existence with its members now generally over the age of 60. My first concert was across the parking lot at a building that no longer exists, Brendan Byrne Meadowlands Area, in December 1983 for AC/DC’s Flick of the Switch show; I was 14. Listed below are my Top 10 favorite concerts of all-time. It seemed prudent to split the eras between vintage concerts and more recent events.

Exhibit 5: Metallica at Met Life, August 4, 2023

Source: Super-Spiked.

Vintage concerts

#10: Van Halen at Madison Square Garden, March 1984

Peak Van Halen. 1984 tour.

#9 Megadeth at Cornell University, April 1988

Megadeth played in the hall where my Psych 101 class was held. Peace Sells tour.

#8 Twisted Sister, Ratt, and Lita Ford at Pier 39, July 1984

An awesome location to see a show. Stay Hungry tour for Twisted Sister.

#7 Iron Maiden at Radio City Music Hall, January 1985

Not too many metal bands have had the opportunity to play Radio City Music Hall. Somehow, Iron Maiden was allowed. I recall the crowd being well behaved by the standards of a 1980s Maiden concert. I also recall it being the night the San Francisco 49ers beat Dan Marino’s Miami Dolphins in the Super Bowl. This was pre-internet era of course. Bruce Dickenson (lead singer) announced the final score.

#6 AC/DC at Brendan Byrne Meadowlands Arena, December 1983

My first concert! Seventh row, center, on the floor. Flick Of The Switch tour.

#5 Slayer at Capitol Theatre in Passaic, January 1987

Reign in Blood is arguably the all-time best death metal album. Slayer took things to another level vis-à-vis the relatively tamer Metallica and Megadeth.

#4 Grateful Dead at Giants Stadium, July 1987

The Dead may seem at odds with the rest of this list, but I was then and still am a fan. It was a blazing hot day at Giants Stadium and I nearly passed out from heat stroke. A friend dragged me to some fire hoses where they were spraying water on fans. Definitely saved me from any risk of something more serious happening health wise. Thank you JH.

#3 Ozzy Osbourne with Metallica at Brendan Byrne, April 1986

This was near peak Ozzy and at a time Metallica was just emerging. Unlike many warm-up acts, people arrived early to catch Metallica on the Master of Puppets tour. I recall James Hetfield having a broken arm, with a crew member filling in on guitar while James still sang vocals. It was only a few months after the untimely passing of bass player Cliff Burton in a bus accident in Sweden.

#2 Metallica at Red Rocks, August 1989

A close runner up to the top pick, I saw Metallica at Red Rocks on the And Justice For All tour. They had a Statue of Liberty replica as part of their set. It started raining and thundering at just about the time the statue comes crashing to the ground as part of the performance. In those days, there were no rain or thunder delays. Metallica powered through. I don’t remember if it stopped raining, and that song was the 12th of 19 played per an internet search. If you haven’t been to Red Rocks, it is one of the best concert venues to see a show.

#1 Judas Priest at MSG, June 1984

My all-time favorite show: Judas Priest at Madison Square Garden in June 1984. Priest is still banned from playing MSG all these years later due to the significant damage done to the arena that evening. I was 15 years old and it was peak Priest on their Defenders of the Faith tour. Fans were ripping the cushions out of the seats and lighting them on fire. Incredibly Priest performed their complete set. I would not have called it a riot, but simply exuberant chaos and a ton of fun (https://ultimateclassicrock.com/judas-priest-madison-square-garden-ban/). Best show ever.

Recent concerts

#10 Black Sabbath at MSG, February 2016

I wasn’t old enough to have caught Sabbath in their early 1970s heyday. A solid re-union effort with Ozzy joining Tony Iommi, Geezer Butler, and a fill-in drummer for a classic set.

#9 Metallica at MetLife, August 2023

It was an effort for the three of us to attend. My friends no longer live in the Tri-State Area and I was returning from a West Coast trip for Veriten. But we are all on the wrong side of 50 and recognize there are only so many more of these opportunities we will realistically get.

#8 AC/DC with Axl Rose at MSG, September 2016

This was during the brief period where Brian Johnson was no longer with the band and Axl Rose of Guns ‘N Roses’ filling in. Axl got AC/DC to play numerous, long forgotten songs. Great show.

#7 Van Halen at PNC Bank Arts Center, August 2015

Glad I got to see Eddie Van Halen one last time before he passed. A throwback set list that largely skipped “pop” Van Halen or Van Hagar.

#6 Megadeth, Suicidal Tendencies, and Children of Bodom at Terminal 5, March 2016

A killer line-up. Suicidal Tendencies’ Lights, Camera, Revolution may be the best album no one’s ever heard of. This was also my introduction to Children of Bodom. Not too many death metals bands incorporate a melodic keyboard.

#5 Children of Bodom with Uncured at Sony PlayStation Theatre, November 2017

Love these mid-size venues. Turns out the warm-up band, Uncured, went to high school with our neighbors’ children which is kind of crazy. Met them in the beer line and noticed how well spoken and polite they were. It wasn’t until I posted a picture that our neighbor saw that we figured this out. Their private school education served them well!

#4 Gojira at Terminal 5, October 2016

For those of you especially concerned about the “urgent climate crisis,” this band is for you! Toxic Garbage Island, Amazonia, and many other Gojira songs have environmentally oriented themes. While Gojira are probably not fans of fossil energy, I believe their musical talent trumps any ill-conceived ideologies they may hold about the importance of all forms of energy.

#3 AC/DC at MetLife, August 2015

With my son when he was 12. His first concert.

#2 U2 at MetLife, June 2017

With my wife and friends…super fun party bus the best way to navigate traffic in and out of Met Life.

#1 Raincheck at 109 (St Andrews), May 2023

Terrific local (St Andrews) college band. Live music in the Home of Golf.